We recently had the pleasure of interviewing Jake Rosser, managing partner of Coho Capital Management. Jake founded Coho in 2007 after working in equity research positions at the value-oriented Auxier Focus Fund and sell-side firm Pacific Crest Securities. He was also a strategy consultant at Alliance Consulting Group. He holds an MBA from Tuck and lives in Portland, Oregon.

The Manual of Ideas: Please tell us about your background and the genesis of your firm. What motivated you to set up your own firm, and how do you envision Coho Capital evolving over time?

Jake Rosser: Curiously enough, I did not discover value investing until after business school. At the time, I was working in strategy consulting and happened to come across The Essays of Warren Buffett. In consulting you spend a lot of time trying to fix broken business models and learn much about what kinds of operating decisions can imperil a company. Buffett’s common-sense approach to assessing the value of a business as well as the simplicity with which he ran the companies within Berkshire Hathaway struck a chord with me. It represented the antithesis to the way most companies conducted themselves. From there, I read the Intelligent Investor and at that point I was hooked.

My route into investment management started with a stint at a boutique investment bank focused on technology, called Pacific Crest Securities, where I was part of the semiconductor research team. While many investors are quick to denigrate the caliber of sell-side research, I found my experience on the sell side invaluable. It gave me a solid foundation for deconstructing company financials and conducting scuttlebutt research. Most importantly, because there is a voluminous amount of writing involved in publishing research it forces one to focus on the fulcrum points of a company’s business model and its investment merits. And surprisingly, given the herd behavior on Wall Street that the sell side helps foster, it helped bring a clarity of focus to my research efforts. This was due to the fact that to be a good analyst on the sell side, one had to truly become an expert in their field of coverage. While now a generalist, that kind of singularity of purpose has served me well in fleshing out the knowledge base for the companies in my portfolio.

After Pacific Crest, I had the good fortune of working for someone whom I consider to be one of the best investors in the world, Jeff Auxier, with the five-star rated Auxier Focus Fund. As the Focus Fund’s only analyst I had the opportunity to examine hundreds of investment opportunities across dozens of industries. Jeff has a profound respect for what risks lie beyond the financials, and he taught me to be a business analyst before a stock analyst. My tenure at Auxier also helped me learn the intense discipline and patience required to wait for the fat pitch to come your way. In the Internet age, one is barraged with so much information, that one’s focus can be obscured. It takes discipline not to get sucked into the chatter. Working with Jeff helped me develop a feel for the extraordinary alignment of events required to create an attractive investment opportunity. They are by nature, rare, so developing a feel for what creates an extraordinary opportunity and enough skepticism to watch hundreds of pitches whiz by the plate is a learned art.

After three years at Auxier, I thought the timing was right to hang my own shingle. The inspiration behind Coho Capital was Mohnish Pabrai. There may have been another investor who brought Warren Buffett’s partnership model into the modern age but I am not aware of one. Unlike the vast majority of investment vehicles, it was clear that Pabrai’s vehicle was designed to make money with his investors rather than off his investors. The ethics of that equation had an instinctive appeal for me.

Like Buffett’s original partnership, Coho Capital is an all-cap fund unconstrained by style boxes and is agnostic with respect to geography. The number and quality of fish one catches is determined by how well stocked their fishing pond is. Our all-cap mandate and lack of geographic confinement allow us to fish from a well stocked pond.

In terms of the evolution of Coho Capital, I hope to expand my partners’ retirement options. If I can deliver on that goal, everything else will take care of itself.

The Manual of Ideas: When it comes to stock selection, what are the key criteria you look for in potential investments?

Jake Rosser: Successful investment outcomes derive from buying the right business at the right price. We have found that more often than not, buying the right business has a much larger outcome on investment returns than buying at an absolute bargain basement price.

Jean-Marie Eveillard And The World's Best Investors by William Green, Barron's Asia

What does it take to achieve enduring success as an investor? A dazzling intellect may help, but it’s useless without the right temperament. In my interviews with many renowned investors, I’ve found that they typically share several indispensable traits, including the independence of mind to go against the crowd, extreme patience and discipline, and extraordinary emotional fortitude.

These winning qualities appear in abundance inThe Great Minds of Investing, a new book on which I collaborated with the photographer Michael O’Brien. The three profiles excerpted here tell the stories of Jean-Marie Eveillard, Francis Chou, and Bill Miller, who have each defied gravity by beating the market over decades. Still, success hasn’t come easy. Miller and Eveillard both suffered excruciating periods of underperformance that almost wrecked their careers. As hedge fund manager Mohnish Pabrai (also profiled in this book) told me, great investors must possess one invaluable characteristic: “the ability to take pain.”

--William Green

Jean-Marie Eveillard

In the late 1990s, Jean-Marie Eveillard faced the investing equivalent of a near-death experience. Amid the insanity of the dotcom bubble, he refused to buy any of the overvalued tech, telecom, or media stocks that were enriching more carefree investors. His most prominent mutual funds, SoGen International and SoGen Overseas, lagged the market disastrously for three years running. “After one year, your shareholders are upset,” he says. “After two years, they’re furious. After three years, they’re gone.” By early 2000, 70 percent of SoGen International’s shareholders had dumped the fund and SoGen’s overall assets had fallen from more than $6 billion to barely $2 billion.

Value investing “works over time,” says Jean-Marie Eveillard, but he had always known that he would suffer from periods of underperformance. Still, he’d never experienced this sustained misery. “You do, in truth, start doubting yourself. Everybody seems to see the light. How come I don’t see it?” As his years in the wilderness dragged on, “there were days when I thought I was an idiot.”

Others agreed. Even his funds’ own board members turned against him, wondering why he had failed to embrace the new paradigm of instant, tech-fueled riches. One executive at his parent company, Société Générale, muttered that Eveillard was “half senile.” At the time, he was only 59. Eveillard thought he might be fired. Instead, the French bank sold his investment operation to Arnhold and S. Bleichroeder for about “5 percent of what it’s worth today.”

And then the bubble burst. The Nasdaq index plunged by 78 percent, devastating legions of reckless speculators. Eveillard’s perennially cautious, value-driven approach was vindicated, and Morningstar later gave him its inaugural Fund Manager Lifetime Achievement Award. His renamed firm, First Eagle Funds, rebounded so strongly that its assets have ballooned to almost $100 billion. Jean-Marie Eveillard retired as a fund manager in 2009, but he remains a senior adviser at First Eagle Investment Management. At 75, he retains his reputation as one of the enduring giants of international investing.

In retrospect, Jean-Marie Eveillard says his feat of trouncing the indexes over three decades was “due largely to what I did not own.” In 1988, when fad-chasing investors were besotted with Japan, he sold the last of his Japanese stocks, unable to find a single company cheap enough to meet his standards. As a result, he emerged unscathed when the world’s second-largest market imploded. Likewise, two decades later, he steered clear of financial stocks before the 2008 credit crisis.

This ability to avoid market mayhem grew directly out of his discovery of Benjamin Graham’s The Intelligent Investor in 1968, shortly after he left France to work for Société Générale in Manhattan. The greatest lesson was that “you have to be humble because the future is uncertain,” says Jean-Marie Eveillard. “Most people refuse to accept that.” For him, this meant buying cheap stocks that provided a significant margin of safety, then protecting himself further by diversifying broadly. Temperamentally, he wouldn’t dare to own a concentrated portfolio, because he was “too worried that it could just blow up” and was “too skeptical about my own skills.” Few professional investors so frequently utter the words “I don’t know.”

(Q) Why did you invest in Chesapeake Energy and what were your reasons to exit ?

Historically based on an energy equivalent basis, crude oil and natural gas prices should have a 6 to 1 ratio. However in the recent years the price of oil typically had traded 8-12x that of natural gas due to a combination of rising domestic production from unconventional shale gas and regulation of natural gas export from U.S depressing price levels and fear premium for the global crude oil prices.

Chesapeake Energy ‘s stock price had hit a low under the leadership of Aubrey McClendon due to unsustainable expansion and spending. Aubrey ran into financial and ethical trouble and was ousted by the board of directors

Chesapeake Energy was going through a change in management with the appointment of Doug Lawler as CEO and election of Carl Icon and Lou Simpson to the board. Doug Lawler had started to bring spending discipline and focus the company on it’s core business.

My expectations and assumptions when I invested in Chesapeake Energy were :

The core business had great underlying assets

There are few shale formation in U.S and there is less possibility of discovering new shale formations

In the long run Natural Gas will do better and there is a high probability that 6:1 ratio between crude oil prices and natural gas are restored.

The U.S govt will be lobbied by European countries to allow Natural Gas exports from U.S ( Though I was not counting on that )

The new management will bring back spending discipline and profitability

Though I still believe in the long term prospects for Natural Gan and Chesapeake Energy, It did not meet all my expectations. When I found a better opportunity to invest capital, I decided to exit Chesapeake Energy.

(.........................

(Q) Why change of heart on India?

Note : This question was in relation to Mohnish’s recent investments in India, which had avoided thus far.

I had stayed away from India as most of the companies tend to be family owned and lots of them have governance issues and hence we didn’t prefer to invest in family controlled businesses.However, we found few opportunities this year, which fit our criteria. One of them is The South Indian Bank.

Why South Indian Bank –

Unlike west or U.S it’s hard to get a banking license in India

60% of the country still don’t have a bank account

Growing middle class are embracing banking and opening bank accounts

It’s not a family owned business

(Q) On re-entry into POSCO

Posco has derived its highly efficient manufacturing process for steel and iron from Nippon Steep, Japan in early 1960’s

Even though Korea has no raw material for steel, due to highly reliable and low cost sea transportation, Posco has developed a strong competitive advantage

Steel business is cyclical and almost all steel companies have losses at one time or another, however Posco has never lost money

Posco has strong support of the South Korean government.

South korean culture and work ethic is also a strong advantage

(Q) How has your process of investment selection changed over time?

Over time i have realized it’s better to be a cloner than to think of original investment ideas.

Using a checklist before making an investment keeps me safe from biases and overconfidence.

(Q) Have you changed your philosophy of portfolio allocation from diversification to concentration over time?

My approach or philosophy depends on the availability of investment opportunities. in 2008-09 there were many opportunities and one could have a diversified portfolio with less than 2-3% allocated to each investment. In the current environment it’s hard to find many opportunities and hence I have changed my allocation to be lean towards concentration.

...............

(Q) How do you read annual reports of tech companies like Google?

I had read the S1 document which Larry Page had written about his vision for Google. It’s important to read the management discussions in the annual reports over the years to get the big picture and understand how the management has executed on it’s vision.

Summarize your investment thesis in a single paragraph and monitor it. If you can’t do that then you can’t own the stock. Do not read the annual report blindly and read it by asking questions.

Based on your research you should be able to extrapolate the range of outcomes for a business in the future.

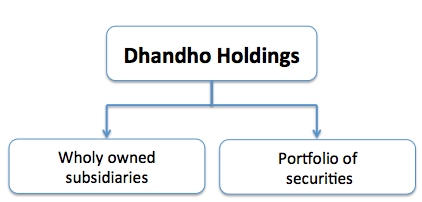

Q&A with Mohnish Pabrai related to Dhandho Holdings

(Q) Recommended Books / Publications on Insurance ?

I've Followed Warren Buffett For Decades And Keep Coming Back To These 10 Quotes by William Green, Obeserver

[buffett]

Fifty years after taking charge of Berkshire Hathaway, Warren Buffett reigns supreme as the greatest investor in history, with a personal fortune of $70 billion. Berkshire’s latest annual report says its market value has soared by 1,826,163 percent under his leadership—an astonishing feat that boggles the imagination.

Warren Buffett and his brilliant partner Charlie Munger are central figures in The Great Minds of Investing, a new book that I’ve written and edited, which will be published on May 29. It features profiles of 33 famous investors, along with portraits by Michael O’Brien, who has traveled all around the world over the past five years to take stunning photographs of Mr. Buffett, Mr. Munger, and the other investors in this book. Many of the great investors I interviewed for the book spoke of Mr. Buffett with awe. For example, Mohnish Pabrai told me that discovering Warren Buffett changed his life, inspiring him to embark on a 30-year “game” in which his goal is to turn $1 million into $1 billion by following what he calls Mr. Buffett’s “laws of investing.”

If you want to get fabulously rich, it clearly pays to study Warren Buffett. But what’s extraordinary to me is that Mr. Buffett’s wisdom goes so far beyond business and investing. Here, then, are ten of my all-time favorite insights from Mr. Buffett on how to build a successful—and happy—life.

"Unconditional Love Is Huge In This World"

In his profile for The Great Minds of Investing, Warren Buffett speaks candidly about the most important reason for his success: the love and support he received from his father, Howard Buffett, a U.S. Congressman whom he revered. “My dad believed in me,” Mr. Buffett explains. “What I basically got from my father is unconditional love. Unconditional love is huge in this world … Whatever I did, he was all for it. It didn’t matter how much money I made or anything like that. It was just, ‘Do your best in whatever you take on.'"

"I Don’t Work To Collect Money."

.......................

What money has bought Warren Buffett is the freedom to live as he chooses. In The Great Minds of Investing, Charlie Munger explains: “Neither of us wanted to be a lowly subordinate in some dominant hierarchy that told us what to do and what to think. That’s why we got the money primarily—because we wanted the independence.”

"Live Your Life by an Inner Scorecard"

In 2008, Mohnish Pabrai and Guy Spier paid $650,100 for a charity lunch with Warren Buffett. Spier, a hedge fund manager based in Zurich, later recalled the meal in his 2014 memoir, The Education of a Value Investor, which I helped him write. What stood out most for him from this three-hour masterclass with Mr. Buffett was one life-changing piece of advice. “It’s very important,” said Warren Buffett, “always to live your life by an inner scorecard, not an outer scorecard.”

Warren Buffett illustrated this by asking: “Would you prefer to be considered the best lover in the world and know privately that you’re the worst—or would you prefer to know privately that you’re the best lover in the world, but be considered the worst?”

A Buffett Disciple On What To Do About Market Turmoil by Guy Spier, Observer

[buffett]

“Back in the day” is an expression I had not heard until I came to Wall Street. To me, it denotes the speaker’s harking back to prior time. A golden age. A time when things were getting better, and what we lacked in experience was made up for by a generally benign and improving environment.

But that it is emphatically not where we find ourselves today. Today life in the markets is hard. Stocks are volatile, and mainly in a downward direction. For the last five years, the world’s Central banks have sloshed vast sums of money into the system, but seemingly to no avail. Because we are most certainly “not out of the woods.” China’s growth seems stalled, commodities are in the tank and uncertainty and loss lurk on every corner, waiting to mug us unsuspecting “babes in the wood.” That is, unless you were smart enough to have bought your own piece of Silicon Valley nirvana in the form of Apple, Amazon, Google and Facebook.

For my part, I wasn’t.

And so we are left with a rush of commentary and analysis that seems to jump out from everywhere. Sometimes I think that more than half the emails in my inbox come from one pundit or another, each one ready with his explanation and what to do about it.

And so what then must we do about our gyrating portfolio values?

A couple of decades ago, the compulsion to do something in my portfolio to “fix things” would have been irresistible: Depending on which combination of commentary and analysis I was most exposed to, I would have wanted to do something like buy portfolio insurance, rotate out of commodities, or find some way to scale into some over-valued and over-hyped sector. Most likely, the panacea would have been a combination of all of these and more.

But that was before I read the Intelligent Investor, invested in Berkshire Hathaway and met Warren Buffett.

Now I know that the best thing to do would be to put the screaming headlines and the rewarmed market commentary aside and simply go for a long walk. Preferably with a dog, or some other good friend, leaving the portfolio entirely alone.

But while I know that this is the right course of action for me, I still find it hard to do. Harder than I ought to find it, given how I have immersed myself in the Graham-Buffett-Munger-Pabrai philosophy of investing and life.

Why is that?

The simple reason is that I have not constructed the best possible environment for myself. Because my repeated experience has been that, no matter how smart I am (or think I am), environment trumps intellect.

Back in 2013 we were invited to attend the Pabrai annual fund meeting to speak to Mr. Pabrai in person. Unfortunately it was not possible to meet him until six days ago. Thanks too my employer Fronteris, I was able to attended his annual meeting and a bike ride with him. In addition to this experience, I was able to meet with other great minds like Guy Spier, Rishi Gosalia (from Google), Haricharan Ramachandra (from Linkedin, who also run the great blog BitsBusiness), Adrian Warner (a fund manager from Australia) and many others.

Highlights:

Score keeping is Mr. Pabrai’s most important lesson to achieve success in life and investing. Especially, the track-record is important in investing and gaming. It can help you to track your mistakes and improve your knowledge.

Has read the Poor Charlies Almanac 7 times and still finds new insights.

Self-improvement is the most important thing, he would bet on the guy with less knowledge and less skills if he has a drive to self-improvement, over a lifetime he will bet the guy with more skills.

Pabrai thinks that Fiat is highly undervalued. Minimum margin of safety is 50% and it has the potential to become a +4x. The spinoff of Ferrari will come in less than a month and it is still not considered in the share price.

Pabrai currently holds: Fiat 42% of the fund , GM B Warrents >10% , POSCO ~10% , ~15% Horsehead Holding , ~10% Google

Dhando Holding IPO will be delayed by 2-3 years, they are currently developing a Smart-Beta value ETF and an own direct small businesses Insurance company (GEICO for businesses)

Stone Trust made an underwriting loss of 4 million this year (when the Equity was just 61 million)

Next, I will share my takeaways from the presentation which was attended by approximately 175 guests:

Start of the presentation

In 1920 there were over 100 car manufactures in the US. It came to a bubble, 10 years later only 3 companies survived. The same happened in the 1960s with the electronic industry and in the 2000s with the internet companies.

He speaks about the “Nifty Fifty” and that investors paid any price for good business in the 1950s. At the end of the day the valuation collapsed and the stocks wend down by 75-90% (featured it in “the mosaic theory as well).

According to Pabrai we are currently seeing the “Nifty-Fifty” again. He mentions Amazon, Tesla, Solar Valley, Uber etc. all are good businesses but are valued way to high. Even the CEO of Netflix says that his stock valuation is crazy.

He compares Tesla with GM, which is currently trading at an P/E of 4x according to him.

He then compares Netflix vs. Micron: Only 3 players in the market of Micron. Micron has a market cap of just 20 Bn. And makes 3,6 bn earnings.

Once every quarter our Mastermind Group gets together over Skype and chats about the current market conditions. We don’t have a strict structure for the meeting. Instead, we shoot for an open forum and discussion of friction points in opinions.

Value Investment: The Approach And Its Applicability by Anton F. Balint

Introduction

This article is designed to give the reader an overview on what value investment is, its establishment and application throughout the years and the reason why it has worked so well. Also, at the end, there will be a reading list with books, articles and other resources for those who want to take it a step further.

The bedrock of value investment

As Oaktree Capital’s Chairman, Marks Howard, put it in an interview with Joel Greenblatt, value means different things to different people. However, generally speaking, value investment is not a strict formula of identifying good investment opportunities but a philosophy – it is a way of viewing investment as a profession and the factors that influence it.

In the library of every value investor there are two books that form the basis of our investment philosophy and strategy: The Intelligent Investorand Security Analysis. The ideas in these holy books of value investment, written by the man who built his fortunes by following the principles presented in them – Benjamin Graham, have been applied rigorously by legendary investors such as Warren Buffett, Joel Greenblatt, Mohnish Pabrai, Peter Lynch and Guy Spier, to name just a few.

Benjamin Graham’s strategy focused on buying bargain stocks, i.e. stocks that traded to a discount to their liquidation value or ‘net nets’ (stocks that traded to a discount to their net value calculated as current assets minus total liabilities). Value investing is by definition a conservative philosophy of investment: it is built on two strong concepts that stood the test of time: ‘intrinsic value’ and ‘margin of safety’. They were created at a time when disclosure of company operations and accounting practices was not as transparent as it is today. It was a time when the American economy has been hit by the 1930s Great Depression and the wealth of many stock market investors was wiped out: a time of panic when reason was no longer king and impulsive decisions took over the investors’ minds and actions. Ben Graham understood these flaws of financial markets and developed a strategy based on mathematical decisions (financial statements’ analysis) and philosophical principles designed to protect his wealth from being wiped out.

However, over time the mathematical strategy put together by Benjamin Graham in Security Analysis, the book that helped Warren Buffett to start his career as an investor, became outdated. Nowadays, it is almost impossible to find stocks that trade at a deep discount to their liquidation value or even book value. Nonetheless, the principles expressed so clearly in his books stood the test of time and proved to work both in times of prosperity and after economic bubbles burst.

Times change but principles are eternal

It is at this point that value investors must be eager to learn and expand the application of these two concepts. One of the greatest additions to the value investment approach, is the work of Philip A. Fisher, the author of Common Stocks and Uncommon Profits and the man that influenced Charles Munger in his investment strategy and portfolio management. Philip Fisher focused on buying good businesses at good prices. He analysed a wide range of qualitative factors such as: the management’s ability to run the organization in a shareholder orientated manner, the company’s dedication to stay ahead of the competition by investing in R&D, the loyalty of its customers and the possibility of new market entrants. It is the idea of buying a quality business at cheap prices that turned Berkshire Hathaway into one of the world’s most valuable companies and that made the partnership between Mr. Buffett and Mr. Munger one of the most successful in financial history. It is also the man that crystalized Warren Buffett’s idea of long term competitive advantage-the moat: buying companies that enjoy large ‘moats’. Of course, identifying the competitive advantages of a company is no easy task and requires a combination of both quantitative and qualitative analysis but the effort pays off.

However, one investor took the ideas of margin of safety and intrinsic value a step further by twitching their application to match today’s market conditions. Before we discuss his contribution to value investment it is important to understand two things. Firstly, the success that Benjamin Graham and his scholars enjoyed by applying his investment strategy mathematically, in other words by analysing company reports and buying cheap businesses, was also due to the fact that the formula resonated with the market’s behaviour and psychology. This does not mean that it aligned itself with the market but on the contraire it worked perfectly to contradict the market in the right way. Secondly, the market’s behaviour is the result of its participants’ actions, more often than not, are impulsive and lack a rational justification: human feelings of panic, fear or hope and excitement take control over the ‘buy and sell’ decisions. As a result, each day the market presents us with a new list of prices that may or may not reflect the real value of the listed companies.

Tobias Carlisle, in his book Deep Value, suggested that buying stocks at a low acquiring multiple (defined as Enterprise Value divided by the Operating Earnings), on the long-term, the investors can cash on extremely good results. Remember, that value investment progressed from simply meaning buying cheap businesses to buying good businesses cheap. Therefore, by using Enterprise Value, the investor takes into account the debt the company has, and the operating earnings will allow the investor to compare the company with other opportunities in a more objective manner: the ‘bottom line’ or net earnings are usually subjected to extraordinary situations – one time losses or gains. Mr. Carlisle’s approach to apply the principles of value investment reflects the current market behaviour and economic conditions and that is why it works: low interest rates, fast access to information and an army of market participants focused on quarterly performance rather than business fundamentals tend to cause mispricing of companies. Of course, having a list of companies that sell at a low acquiring multiple will not guarantee above average returns: as value investors we are sceptical and we like to find the intrinsic value of our stocks. Therefore, a thorough analysis of the business, from its reports to its management’s attitude and consumer confidence, is necessary in order to make an investment decision.

These are just two of the many possible ways one can apply the principles of intrinsic value and margin of safety. Moreover, value investment, as a philosophy, shaped the meaning of various financial terms – like goodwill. Warren Buffett in a letter to shareholders in 1983, made the difference between accounting goodwill (the premium paid for the identifiable assets of a business when it is acquired that is then added in the balance sheet as an asset whose value decreases with time) and economic goodwill (the capitalized value of the excess return a company is believed to produce in the future). The arcane nature of these concepts can put many investors off. However, from a value investor’s perspective, you want to purchase businesses with a lot of economic good will and be warry of those that have their accounting goodwill as a vast proportion of

Get the entire 10-part series on Charlie Munger in PDF. Save it to your desktop, read it on your tablet, or email to your colleagues.

“We don’t give a damn about lumpy results. Everyone else is trying to please Wall Street. This is not a small advantage.” - Charlie Munger

You will underperform. That’s right I said it!

We will all underperform at multiple points while investing in the stock market. I hate to break it to you, but it’s an inevitable fact of life that we will underperform the market from time to time — and it’s perfectly ok!

It’s a “Catch-22” in some sense — to outperform and compound capital at high rates over time, underperformance is a necessity.

If you want to beat the average index, you have to deviate from the index — it’s a simple concept, but far from easy to execute. It can be stressful and a hindrance when we deviate from the index during the short term. However, we gain a significant advantage long-term from this deviation. There are numerous investors who produced investment returns that are multiples over that of various indices. The only way they can accomplish this is by owning a portfolio that looks nothing like the index.

We believe in concentrating our best ideas into a focused portfolio. We want to own the cheapest, highest quality stocks with the best future. I have no idea whether these investments will rise today or tomorrow (BTW, no one does). However, I’m very confident that this strategy will work incredibly well over time.

The psychological pressure to succeed long-term in investing can be tough for most individuals.

Investors must stick to a long-term, rational system. We should consider ourselves lucky. By its very nature, the stock market shifts capital to the patient investor from those who are impatient and active.

WE WILL UNDERPERFORM. And you should welcome those periods from time to time. EVERY great investor will have periods of underperformance. Unfortunately, these periods can be longer than anticipated before the investor is proven correct for their patience. The problem is we only hear about the underperformance from the media because it causes more of an emotional feeling of loss for individuals. This tactic follows the closely held mantra in the media, ‘if it bleeds, it leads. ‘

These great investors have been vilified by many in the media for underperformance for a month or a quarter or even a year. They’ll say that they’ve lost touch with reality, or they’re missing the next great investment “revolution” or trend. I’ve heard this many times before from Warren Buffett “missing” the great and ever-growing tech rally in the late 1990s to Bruce Berkowitz after the financial crisis when he invested in AIG and many of the bailed out banks. In the case of Berkowitz, these investments went on to make him and his investors multiples on their investments.

All the great’s have fallen from favor or replaced by those who are popular today, from Warren Buffett, Charlie Munger, Ruane Cunniff, Bill Miller, Bruce Berkowitz, Mohnish Pabrai, and Mason Hawkins —They’ve ALL underperformed for periods at a time.

We never focused on short-term performance (>3 years). Following a proven value investing process in a focused manner will likely lead to outperformance over time vs. indices or your competition. It’s brought us success, and it should bring success to many other as well.

If you haven’t embarked on this investing philosophy just yet…be careful. It’s vitally important that you understand and can combat certain psychological nuances that are likely to make you feel very uncomfortable at times. We discuss many of the mindsets and philosophies to focused investing in our book, Value Investing Edge (this is not a shameless plug, buy it if you want…if you don’t, it’s no skin off our backs. Regardless, we think it will be a welcome addition to any value investor’s library). Whether you purchase the book or not, understanding your philosophy, and the principles that come with that philosophy, can have a profound effect on your success long-term as an investor.

Investors should always ask themselves whether these principles make sense? Are they rational? Are they scalable and able to last the test of time? Has this process been successful in the past? Is the process likely to do well in the future?

In addition to improving my process over the years, I’ve spent a great deal of time focusing on putting myself in the right type of environment which will allow me to be uninfluenced and patient in my investing. I was fortunate enough to manage money in the US Virgin Islands for five years, and now I find myself in Charlotte, North Carolina.

Very different places to be sure. However, both offer the sanctuary I seek for the right type of environment to keep me focused on my long-term process. My checklists, my watch lists, and my environment have helped me tremendously over the years with investing in opportunistic, contrarian investment ideas that I can use in a focused manner for our portfolios.

Never has the road to wealth been one of “what’s popular today.” We stay away from these short-term trading vehicles with great stories and no earnings. We focus instead on high-quality businesses at reasonable prices (or special situations). This process takes patience and discipline, as well as being independent in your thinking.

I feel incredibly lucky to have you as one of my subscribers and readers. I look forward to continuing to earn your trust and friendship.

Get The Full Warren Buffett Series in PDF

Get the entire 10-part series on Warren Buffett in PDF. Save it to your desktop, read it on your tablet, or email to your colleagues.

ABOUT THE AUTHOR:

Lukas Neely is a former Hedge Fund Portfolio Manager and author of the Amazon #1 bestselling book (valuation), Value Investing Edge: A Value Investor’s Journey Through The Unknown. His work has been cited on such sites at TED, Wall Street Journal, Bloomberg, ValueWalk, CBS, GuruFocus, and Seeking Alpha. He is also the co-founder of Vantage Research, the provider high-quality investment idea generation, serving investment funds, portfolio managers, and sophisticated investors.

Feynman Investment Research LLC is an independent investment research firm that focuses upon providing actionable and timely investment ideas on undervalued and under- recognized companies.

In this interview, we will be chatting with Brian Grosso. Grosso is currently finishing up his senior year of undergrad and jumping right into the investment business, as an investment advisor at Rugged Group, LLC, that he recently formed. I met Brian 3-4 years ago, on an investment blog on Facebook, when we were both beginning our trek down the road of investing. Since then we have bounced investment ideas off each other and have chatted multiple times. Grosso has a passion for investing, is very skilled at analyzing companies, has deep insight and understanding of business and is way ahead of many of his peers, given how young he is.

Feynman Investment Research Interviews Brian Grosso

So Brian, tell us about yourself (school, work, hobbies, etc.)

Brian Grosso: Sure Nick, Thanks for interviewing me!

I’m currently in my senior year at the University at Buffalo and will graduate with a degree in Accounting in the spring. This past summer, I interned at a large bank, which gave me a lot of perspective on Corporate America and my own personal work preferences. I’d been thinking about the possibility of opening an advisory business for several years at that point, but the internship experience and some discussions with a key mentor catalyzed me to go through with my plans. Rugged Group LLC was formed in early August and we are now over the regulatory hurdles and doing business.

As for hobbies, I really enjoy reading, walking, hiking, and spending time with family (not necessarily in that order!), as well the occasional obsession with Zynga Poker.

Has an accounting background helped you with analyzing companies? What major would you suggest aspiring student investors to jump into?

Brian Grosso: An accounting background has definitely helped. I would recommend accounting to prospective investors. Accounting is necessary to understand how businesses are performing and what they are worth. Learning accounting has led me to be much more skeptical of GAAP accrual basis numbers, because there is a good deal of discretion and assumptions involved in those numbers, and it is certainly not the only way to report results. In fact, GAAP has changed over time, if that says anything about its infallibility.

Here is a brief example of how GAAP results can be distorted. When a company has a defined benefit retirement plan for its employees (read: pension), it creates both an asset and liability. The assets are tangible – the securities that the plan actually owns such as bonds and stocks that it is trying to earn a return on. The liabilities are not – they are projected future cash outflows to employees the company will have to pay out, discounted back to the present using a discount rate. Clearly a lot of assumptions are involved and one that is problematic is the discount rate that is used. The discount rate that actuaries normally use is interest rates on high quality (AAA, AA, etc) corporate bonds. When interest rates get very low as they are now, the discount rate is very low (like 3%), and in turn the present value of the liabilities skyrockets without any change in what actually must be paid out in the future.

In reporting the plan on the financial statements, the plan assets and liabilities are netted together to get a net asset or liability. In this low-rate environment, many companies have very large pension liabilities that investors perceive as debt and are including in enterprise value calculations, but the crazy thing is that if interest rates increase 100bp or so, many of these liabilities will vanish without any fundamental change at the company. Having learned accounting, I’m much more aware of these kinds of nuances and since much of accounting is principles, if I come across a nuance that I’ve not learned directly, I can often still put the pieces together from what is disclosed in the footnotes.

That is really interesting in regards to GAAP EPS. I always use FCF myself when valuing companies, but never knew that there was an issue with GAAP when it comes to pension plans. I can really see how an accounting background has been of value to you. How did you end up picking Rugged as a name for your advisory business (I am sure it has some meaning)?

Brian Grosso: Great question. Rugged has two meanings. The first is a rough, uneven surface that is difficult to traverse. Think rugged terrain. I think this is symbolic of financial markets, or at least the way I want myself and clients to think about them. The journey to wealth through stock ownership is not an easy, straight, or paved path. There are ups and down. Big ups and downs. And it’s tough. Which brings us to the second meaning of the word rugged: strong, tough, resilient or determined in the face of challenge or hardship. These are qualities that the rugged financial terrain demands of investors. You need to be unfazed in the face of the big moves. The big red days that keep you up at night. That is hardship that needs to be overcome.

That’s a salient metaphorical name for an advisory business in relations to the overall pendulum swings of the stock market. I’ve always liked names of advisory businesses that had meaning to them, instead of just someone’s first or last name. What attracted you to the investing world?

Brian Grosso: After graduating from high school, I still didn’t really know what career I wanted to pursue. I was set to enter college as an engineering major. Early in the summer, I stumbled across some articles on Buffett and value investing. It’s funny – I had some savings from working part-time in high school and vividly recall googling “best investment strategy.” Information begot information (the internet is a wonderful thing) and I’m still digging into this endless chain of information today.

That sounds a lot like how I ended up getting into investing, I was also the same in regards to not knowing what to pursue as a career. Could you elaborate upon your investment style?

Brian Grosso: I’m a bottom-up value investor. I go through screens of mostly small, cheap stocks looking for situations where:

I understand the business

I expect annual returns over the next 3-5 years of at least 20-25% from the stock

An adverse outcome does not seem to imply I am losing money, or as Mohnish Pabrai would say, “Tails, I don’t lose much”

I’m a firm believer that the future is uncertain and the way I approach valuation reflects that. There is always more than one potential outcome and I model returns for each, and then assign probabilities to get an expected return. I’ve also noticed over time that many of my worst decisions have been made very quickly, so I am trying to slow down my decision-making process through the use of watch-lists, articles, and starter positions as means of delaying gratification.

That is interesting how you have a process to delay the gratification of investing into company too fast. I

The Pabrai Funds – the hedge funds managed by value investor Mohnish Pabrai — saw the value of their assets fall by 19% during 2015 according to the firm’s fourth quarter and full-year 2015 letter to investors, a copy of which has been reviewed by ValueWalk.

This high double-digit loss has curbed the Pabrai Investment Funds’ gains since inception, but overall returns since inception are still eclipsing those of the benchmark indices. Since inception, the Pabrai Investment Funds have produced a cumulative net return of 535.2% for investors, or 12.9% annualised compared to a return of 4.4% on an annualised basis the S&P 500 and a cumulative return of 91.6%.

One holding was responsible for all of Pabrai Investment Funds’ losses for 2015. Excluding the losses incurred by this position, the funds would have been flat for the year.

Horsehead Holdings was originally acquired by the funds back in 2008 as a traditional Benjamin Graham investment. At first, the stock produced a great return of the fund appreciating by over 400% in less than 13 months. And after conducting further due diligence on the company, Pabrai became impressed with Horsehead’s management and continued to hold the company even after its impressive gains.

Horsehead’s growth continued, and the company made a number of sensible acquisitions at attractive prices. Pabrai writes that he, “carefully studied all of Jim’s major capex decisions and execution skills. They were flawless. These new businesses were nicely integrated.”

Pabrai Funds: Keep buying

Horsehead ticked all the boxes on Pabrai’s investment checklist, and as a result, his funds continued to buy the stock. Then in 2011 Horsehead decided to transition zinc production from its 80-year old smelter to using a different chemical process to produce zinc. The new plant was expected to cost about $350 million and increase EBITDA by as much as $110 million making the company one of the lowest cost zinc producers on the planet. This new plant, coupled with a captive low cost “EAF Dust Mine” that basically never depletes ticked all the boxes for sound long-term investment and when completed would position Horsehead for long-term growth.

Unfortunately, executing this almost perfect plan has turned out to be harder than anyone expected. Costs have risen to $500 million and after 18 months, the plant was only running a 25% capacity. At the end of January, Horsehead needed another $100 million to cover losses while the plant ramped up to full production. As costs have soared, zinc prices have collapsed. Pabrai wrote his 2015 letter to investors in mid-January and around a month after Horsehead filed for Chapter 11 after running into severe liquidity issues.

But does Pabrai consider Horsehead to be a mistake? No, what he believes to be a mistake is buying over 4.9% of the shares outstanding:

“The mistake was buying over 4.9% of the shares outstanding. In the last 16+ years at Pabrai Funds, we have bought over 5% or even over 10% of a few public companies. In no cases have we ever ended up with a winner” — Mohnish Pabrai full-year 2015 letter to investors

He continues:

“If we owned less than 4.9% of Horsehead, it is almost certain we would have done tax loss selling in 2015 at significantly higher prices – and decided not to buy it back based on all the updated current facts. We are going to endeavor to never ever go over 4.9% anymore on any stock in the US. Been there. Done that. Got the T-shirt.”

And finally:

“Looking back at all the available information, I would still have made the investment (though we’d have maxed out at $35 million invested).”

Pabrai Funds – Mistakes are part of investing

The Horsehead debacle is a great experience for both Pabrai and outside investors alike. Mistakes and losses are part of the investment landscape, and while the losses booked as a result of Horsehead’s collapse into bankruptcy have hit returns, the Pabrai Funds still have an attractive batting average. Sir John Templeton often remarked that his investment analysis was proved wrong about 1/3 of the time. Since 2010, Pabrai Funds has a right to wrong ratio of 511:136 or about 3.76:1.

“The goal is to always try to get realized losses to be as close to zero as possible.” — Mohnish Pabrai full-year 2015 letter to investors

4 Things Billionaire Investors Have In Common – Part 2:Asymmetric Risk/reward by Lars Christian Haugen

This is part 2 of a four part series of short articles (click here to read part 1). Each article sets out to explain an important trait that billionaire investors have in common. The goal of these articles is to explain simple concepts that the best investors in the world use, that you can implement today. Success leaves clues and one of the best ways to learn is to deconstruct and reverse engineer what the best in the world do. So let’s get to it.

Get The Timeless Reading eBook in PDF

Get the entire 10-part series on Timeless Reading in PDF. Save it to your desktop, read it on your tablet, or email to your colleagues.

“Superficially, I think it looks like entrepreneurs have a high tolerance for risk. But one of the most important phrases in my life is ‘protect the downside’”. – Richard Branson

“To make a lot of money, you have to take a lot of risk”. How many times have you heard that phrase?

It’s something I had heard often and I accepted it because it seemed to make sense. However, I realized that billionaires don’t think this way. They are obsessed with risking a little to make a lot, so-called asymmetric risk/reward. Warren Buffett has a different way of explaining it: only swing at the fat pitches. And it’s what famous fund manager Mohnish Pabrai quips “heads I win, tails I don’t lose much”.

This is a simple, yet very important concept, so I thought it deserved some looking into.

Below I will show you three examples of billionaires who risked a little to make a lot. My goal is that after reading these examples you will change the way you look at risk/reward and consequently make better investing decisions. This thinking has helped me because I found myself making bad investments because I was impatient and wasn’t willing to wait for the fat pitch.

The first example is of a guy who made $4 billion personally on what has been called “the greatest trade ever”.

The Greatest Trade Ever

In 2009 Greg Zuckerman published a book called "The Greatest Trade Ever" where he chronicled how hedge fund manager John Paulson made out like a bandit during the subprime mortgage crisis.

According to Zuckerman, Paulson’s hedge fund made $15 billion in 2007. Paulson made nearly $4 billion personally. Apparently, it was the largest one-year pay out in the history of the financial markets. Below is a chart showing the monthly return of Paulson’s hedge fund. You should note that in the investing industry, a 15% annual return is seen as very good. A 20% annual return is extraordinary:

Source: Wall Street Journal

Billionaire Investors

In July of 2007 Paulson made 76% alone! And in several of the other months his return was multiples of what a great hedge fund can hope to make in a year. You might think that he had to risk a lot to get these returns, but that’s not the case. According to Zuckerman he only had to risk 8% per year to enter the trade. His downside was 8%, while his upside was several hundred per cent.

Zuckerman tells a funny story about Paulson’s analyst who discovered the trade (it was not Paulson himself who discovered it). After the dust had settled from the subprime crisis and Paulson’s fund made all that money, the analyst was on vacation with his wife.

His wife stopped by an ATM and checked the balance of their checking account. The number that appeared on the screen was a handsome $45 million. The money had recently been deposited in their account and it was the bonus for discovering the trade.

Not a bad payday for finding one trade.

A very impressive part of Paulson’s accomplishment was that he wasn’t even a real estate investor. And he didn’t even discover the trade, it was his analyst. So how the hell was a guy who didn’t even specialize in real estate able to pull off the greatest trade in history?

It’s because he looked at the world differently, and he sought out to structure trades that would limit his downside, and give him a huge upside. Most of the people he presented the idea to did not believe in the trade. Some even considered pulling their funds. The trade and its structure were too unconventional for normal investors to accept. But by definition asymmetric risk/reward trades need to be unpopular, or else they would not be asymmetric.

The Billionaire Who Bought 20 Million Nickels

Another hedge fund manager that made his name during the subprime crisis is Kyle Bass, who reportedly made a return of 212% in 2007. He was actually one of the people that Michael Lewis interviewed for his book “The Big Short”, but Bass was left out of the book in the end (however, he was portrayed in Lewis’ next book “Boomerang”).

Bass is another billionaire who looks at the market differently than the average investor. On his subprime trade he reportedly only risked 6 cents to make 100 cents. That’s almost a 17-1 risk/reward. I have to admit that I didn’t even know those type of investments existed.

After his subprime success he took it one step further. He asked himself “how can I find an investment that has no risk”?

He found it in nickels…..yep, nickels. He reportedly made a $1 million investment in nickels, i.e. he bought 20 million coins.

You’re probably wondering: “how in the world is that trade supposed to pay off”?

Well, according to Bass it takes the government almost 10 cents to produce a nickel. And the material that is in the coin is worth 6.8 cents. He concluded that eventually the government has to stop producing these coins, because they can’t continue making something that costs twice as much as it’s worth.

Bass makes the point that from day one the asset you are buying is already worth 36% more than you paid for it (it costs 5 cents, but the value is 6.8 cents). And there is no downside because a nickel will never be worth less than 5 cents.

And when the current version of the nickel is eventually stopped being produced, these coins will increase in value (because of scarcity). This apparently happened with the penny.

According to this article almost all pennies made before 1982 are made up of 95% copper and 5% tin and zinc. In 1982 the US Mint changed the composition of the penny because it was too expensive to produce the penny from copper. Pennies now have the current mixture of 97.5% zinc and 2.5% copper. Today, the amount of copper in an old penny is worth a little more than 2 cents. That’s a 100% premium on the face value of the penny.

Apparently pennies that are out of date can be worth quite a lot of money. According to this list, pennies can fetch anything from $1 to $1,200 (a value that is 120,000 times the original value!).

Most people would probably not look for trades that have no downside risk, while having a guaranteed upside. And they would definitely not go out and buy 20 million nickels. But that’s what sets billionaires like Bass apart from the rest of us.

We recently had the pleasure of interviewing Jake Rosser, managing partner of Coho Capital Management. Jake founded Coho in 2007 after working in equity research positions at the value-oriented Auxier Focus Fund and sell-side firm Pacific Crest Securities. He was also a strategy consultant at Alliance Consulting Group. He holds an MBA from Tuck and lives in Portland, Oregon.

Get The Timeless Reading eBook in PDF

Get the entire 10-part series on Timeless Reading in PDF. Save it to your desktop, read it on your tablet, or email to your colleagues.

Q&A with Jake Rosser

The Manual of Ideas: Please tell us about your background and the genesis of your firm. What motivated you to set up your own firm, and how do you envision Coho Capital evolving over time?

Jake Rosser: Curiously enough, I did not discover value investing until after business school. At the time, I was working in strategy consulting and happened to come across The Essays of Warren Buffett. In consulting you spend a lot of time trying to fix broken business models and learn much about what kinds of operating decisions can imperil a company. Buffett’s common-sense approach to assessing the value of a business as well as the simplicity with which he ran the companies within Berkshire struck a chord with me. It represented the antithesis to the way most companies conducted themselves. From there, I read the Intelligent Investor and at that point I was hooked.

My route into investment management started with a stint at a boutique investment bank focused on technology, called Pacific Crest Securities, where I was part of the semiconductor research team. While many investors are quick to denigrate the caliber of sell-side research, I found my experience on the sell side invaluable. It gave me a solid foundation for deconstructing company financials and conducting scuttlebutt research. Most importantly, because there is a voluminous amount of writing involved in publishing research it forces one to focus on the fulcrum points of a company’s business model and its investment merits. And surprisingly, given the herd behavior on Wall Street that the sell side helps foster, it helped bring a clarity of focus to my research efforts. This was due to the fact that to be a good analyst on the sell side, one had to truly become an expert in their field of coverage. While now a generalist, that kind of singularity of purpose has served me well in fleshing out the knowledge base for the companies in my portfolio.

After Pacific Crest, I had the good fortune of working for someone whom I consider to be one of the best investors in the world, Jeff Auxier, with the five-star rated Auxier Focus Fund. As the Focus Fund’s only analyst I had the opportunity to examine hundreds of investment opportunities across dozens of industries. Jeff has a profound respect for what risks lie beyond the financials, and he taught me to be a business analyst before a stock analyst. My tenure at Auxier also helped me learn the intense discipline and patience required to wait for the fat pitch to come your way. In the Internet age, one is barraged with so much information, that one’s focus can be obscured. It takes discipline not to get sucked into the chatter. Working with Jeff helped me develop a feel for the extraordinary alignment of events required to create an attractive investment opportunity. They are by nature, rare, so developing a feel for what creates an extraordinary opportunity and enough skepticism to watch hundreds of pitches whiz by the plate is a learned art.

After three years at Auxier, I thought the timing was right to hang my own shingle. The inspiration behind Coho Capital was Mohnish Pabrai. There may have been another investor who brought Warren Buffett’s partnership model into the modern age but I am not aware of one. Unlike the vast majority of investment vehicles, it was clear that Pabrai’s vehicle was designed to make money with his investors rather than off his investors. The ethics of that equation had an instinctive appeal for me.

Like Buffett’s original partnership, Coho Capital is an all-cap fund unconstrained by style boxes and is agnostic with respect to geography. The number and quality of fish one catches is determined by how well stocked their fishing pond is. Our all-cap mandate and lack of geographic confinement allow us to fish from a well stocked pond.

In terms of the evolution of Coho Capital, I hope to expand my partners’ retirement options. If I can deliver on that goal, everything else will take care of itself.

The Manual of Ideas: When it comes to stock selection, what are the key criteria you look for in potential investments?

Jake Rosser: Successful investment outcomes derive from buying the right business at the right price. We have found that more often than not, buying the right business has a much larger outcome on investment returns than buying at an absolute bargain basement price.

To that end, we focus first on appraising the value of the business. This starts by reviewing the industry in which the company operates. There are many industries we will give a pass simply because the economics are unattractive. This is typically true of industries that are capital intensive, exhibit low barriers to entry, possess unionized work forces or are characterized by a lack of pricing power.

Shipping, grocers or mining for example are not industries that would meet our requirements. We try to not be too dogmatic in our approach, however, and recognize that even in unattractive industries, a superb management team with superior capital allocation abilities can trump poor industry economics. Wilbur Ross in steel or coal mining would be one example. Another example would be the management teams of Markel (MKL) and Aspen Insurance (AHL), which we own in the fund, in the commoditized insurance industry. On balance though, we subscribe to the Buffett adage that “when a management team with a reputation for brilliance tackles a business with a reputation for bad economics, it is the reputation of the business that remains intact.”

In assessing industries, we also want to make sure we understand the industry enough to make informed judgments on competitive dynamics. Industries with ephemeral market leaders, such as technology, often get thrown in the too hard pile. To have enough conviction to hold a stock when the market is moving against you, you have to be able to understand it, which is why we endeavor to remain within our circle of competence.

Assessing industry dynamics before drilling down on the business helps us think like an owner. Like all value investors we view a stock purchase as fractional ownership in a business. We want to judge the staying power of that business before committing capital to it. As part of that effort we spend a lot of time searching for companies that have some type of competitive moat affording the company pricing power. Next, we attempt to understand how durable that moat is. We examine how businesses have fared across economic cycles and assess trends in margin structure for any clues that either refute or strengthen our conviction. Such an approach results in a list of the world’s best businesses.

These businesses are rarely cheap, however, so we are

,

,

discuss the parallels between investing and the game of bridge.

discuss the parallels between investing and the game of bridge.